Tags

credit default swaps derivatives, cricketdiane, financial crisis, financial derivatives, financial regulation reform, US economic crisis, Wallo Street, world economic crisis

SEC explains dangerous derivatives – video (CNN)

<object width=”384″ height=”356″ classid=”clsid:D27CDB6E-AE6D-11cf-96B8-444553540000″ id=”ep”><param name=”allowfullscreen” value=”true” /><param name=”allowscriptaccess” value=”always” /><param name=”wmode” value=”transparent” /><param name=”movie” value=”http://i.cdn.turner.com/money/.element/apps/cvp/4.0/swf/cnn_money_384x216_embed.swf?context=embed&videoId=/video/markets/2010/03/04/mkts_ss_sec_white_board.cnnmoney” /><param name=”bgcolor” value=”#000000″ /><embed src=”http://i.cdn.turner.com/money/.element/apps/cvp/4.0/swf/cnn_money_384x216_embed.swf?context=embed&videoId=/video/markets/2010/03/04/mkts_ss_sec_white_board.cnnmoney” type=”application/x-shockwave-flash” bgcolor=”#000000″ allowfullscreen=”true” allowscriptaccess=”always” width=”384″ wmode=”transparent” height=”356″></embed></object>

Link –

http://money.cnn.com/video/markets/2010/03/04/mkts_ss_sec_white_board.cnnmoney/

from

http://money.cnn.com/2010/04/21/news/economy/derivatives/index.htm?source=cnn_bin&hpt=Sbin

**

My Note –

After watching this three times – it occurred to me that, from short selling to derivatives to hedge funds to any number of financial products intended to mitigate risks – all are making money only when the business, company, loan, commodity or country fails. Therefore, the goal becomes the failure of the target rather than its success. Apparently it has been very successful in making money that way. However, it is exactly the opposite of encouraging, creating, sustaining or setting a foundation for good, healthy, profitable businesses, industries, trades, stocks, profits, assets, commodities, treasuries or anything else, in fact.

Every part of the process whereby money is made betting on the failure rather than the success of businesses, would inherently pursue those failures with every tool, strategy and purpose of the plays that could be made. It would encourage every shady practice from gossip to undermine the value or belief in the values of a company; to lobbying shareholders and others; to re-defining values through media outlets and publicity; to discouraging solvency or any re-working of loans, obligations and business practices to have solvency. And all this has happened and by nature would happen because the goal which makes money in the case of short selling, hedge funds, risk mitigation products and credit default swaps / financial derivatives is the ultimate and untimely destruction of the companies that are their targets.

So, making money based on failure. Once a credit default swap is taken out as insurance then the most immediate and predictable financial reward comes from the failure rather than the success of the company to pay back the bonds, loans or continue profitably. Does that also mean banks get more money by defaults and foreclosures than they could ever hope to recoup from working with the homeowners to keep their houses as well? It reminds me of the junk bond traders in the eighties that raided companies after leveraging junk bonds that weren’t worth the paper they were printed on in order to acquire the company in the first place. Everything that is designed to profit when others fail is sure to encourage that failure more quickly and efficiently with as great an immediate gain to the outsider gaining by that failure as possible. But, doesn’t that destroy the integrity of the overall system and undermine the real value of tangible assets? And wouldn’t it eventually make every business and business asset toxic as well?

– cricketdiane

**

04-22-10 Producer Price Index from Cleveland Fed website –

(chart included below in post)

Food prices jumped up 32.5 percent in March, accounting for “over 70 percent of the increase” in the overall index according to the BLS. Energy prices also rose during the month, increasing 9.1 percent following a 29.6 percent decline in February.

http://www.clevelandfed.org/research/data/updates/past_detail.cfm?m=4&y=2010

***

Obama urges finance-sector reform support

UPI

Obama: Wall St., D.C. share blame

CNN

**

(excerpt from)

Big banks mint money again: $18.7 billion

By Colin Barr, senior writer

April 21, 2010: 4:28 PM ET

(Fortune)

The top five bank holding companies in derivatives – JPMorgan, BofA, Goldman, Morgan Stanley and Citi – hold $280 trillion worth of notional derivatives contracts, according to the Office of the Comptroller of the Currency. That’s 20 times the gross domestic product of the U.S.

Fisher cited a study by Bank of England financial stability watchdog Andrew Haldane disputing the supposed economic benefits of giant banks. Fisher and Haldane both noted that the cost of the government’s implicit support of the biggest institutions runs well into the billions of dollars annually.

Among other things, access to cheap funds enables the giant banks to grow at the expense of smaller, nimbler, more community-focused lenders, which would be more apt to lend to small businesses than devise new ways to separate clients from their money.

In this view, the giant trading books that are now fueling big bank profits also help to make managing or regulating the giant banks essentially impossible.

“When Lehman Brothers failed, it had almost one million open derivatives contracts – the financial equivalent of Facebook friends,” Haldane wrote. “Whatever the technology budget, it is questionable whether any man’s mind or memory could cope with such complexity.”

Just as it’s questionable whether big profits at the big banks are worth celebrating.

http://money.cnn.com/2010/04/21/news/companies/bigbanks_profits.fortune/index.htm

Industrial Production and Leading Indicators Chart through January 2009

this chart came from my files but I’m not sure where I originally found it and I apologize for that but will find the source later and include it here. – cricketdiane

***

Index comparison of consumption ( comparing countries) - Institut de Statistiques through May 2009

(from)

**

english.ctei.gov.cn/Headlines/222528.htm

Growth Rate of Total Industrial Production Value and Sales Value - Textile Industry China - National Bureau of Statistics of China

***

US Industrial Production 2009 - Source - Federal Reserve Board

http://www.clevelandfed.org/research/data/updates/past_detail.cfm?m=12&y=2009

**

FROM THIS YEAR – 2010

- 04.22.2010

- PPI

-

- The Producer Price Index for finished goods rebounded from a 6.5 percent (annualized rate) decrease in February, jumping up 8.4 percent in March. Food prices jumped up 32.5 percent in March, accounting for “over 70 percent of the increase” in the overall index according to the BLS. Energy prices also rose during the month, increasing 9.1 percent following a 29.6 percent decline in February. Excluding volatile food and energy prices, the “core” PPI was virtually unchanged in March, rising just 0.7 percent, and is up 1.9 percent over the past three months. Over the past 12 months, the headline PPI is up 6.0 percent, but the core PPI is up a paltry 0.9 percent. Further back on the line of production there was some evidence of pricing pressure, as core intermediate goods prices increased 9.1 percent and core crude goods prices jumped up 101 percent. Over the past 12 month these volatile series are up 4.0 percent and 44.6 percent, respectively.

http://www.clevelandfed.org/research/data/updates/past_detail.cfm?m=4&y=2010

**

Derivatives: Largely an insiders’ game

http://money.cnn.com/2009/07/23/news/economy/derivatives_insider_game.breakingviews/index.htm?postversion=2009072405

Derivatives: The risk that still won’t go away

http://money.cnn.com/2009/06/22/news/economy/derivatives_regulation_risks.fortune/index.htm?postversion=2009062410

Good news, bad news on derivatives

http://money.cnn.com/2009/06/26/news/derivatives.drop.fortune/index.htm?postversion=2009062614

(from)

http://money.cnn.com/2010/04/21/news/economy/derivatives/index.htm?source=cnn_bin&hpt=Sbin

* Obama asks Wall Street to back reform

http://money.cnn.com/2010/04/22/news/economy/Obama_Wall_Street_reform/index.htm?source=cnn_bin&hpt=Sbin

* The real outrage is how CEOs are paid

http://money.cnn.com/2010/04/22/news/companies/executive_compensation.fortune/index.htm?source=cnn_bin&hpt=Sbin

* Detroit’s small business allure Video

http://money.cnn.com/video/smallbusiness/2010/04/20/sbiz_detroit_start_business.cnnmoney?source=cnn_bin&hpt=Sbin

* Untangling Wall Street’s tricky bets

http://money.cnn.com/2010/04/21/news/economy/derivatives/index.htm?source=cnn_bin&hpt=Sbin

Morgan Stanley easily tops estimates

http://money.cnn.com/2010/04/21/news/companies/morgan_stanley/index.htm?postversion=2010042112

**

Personal Income - Percent Change - from US Bureau of Economic Analysis

***

- 04.08.2010

- Fourth District Employment Conditions

-

- The Fourth District’s unemployment rate increased 0.2 percentage point to 10.4 percent for the month of February. The increase in the unemployment rate is attributed to an increase of the number of people unemployed (1.9 percent) and an increase in the labor force (0.2 percent).The distribution of unemployment rates among Fourth District counties range from 7.5 percent (Butler County, Pennsylvania) to 20.8 percent (Magoffin County, Kentucky), with the median county unemployment rate at 11.4 percent. These county-level patterns are reflected in statewide unemployment rates as Ohio and Kentucky have unemployment rates of 10.9 percent and 10.9 percent, respectively, compared to Pennsylvania’s 8.9 percent and West Virginia’s 9.5 percent.

http://www.clevelandfed.org/research/data/updates/past_detail.cfm?m=4&y=2010

**

All governments need to act. Measures to clean up the banks and revive the housing market in the United States are an important part of the solution, and are needed urgently. But they are no longer enough.

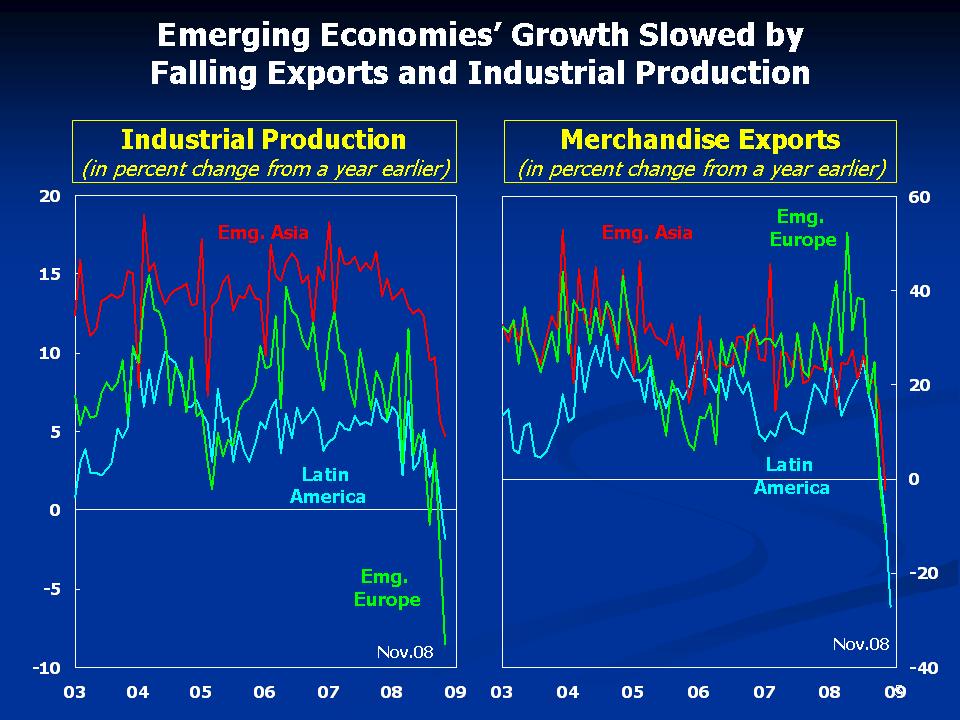

This is because the crisis is now much broader, and it is having profound effects on both advanced and emerging economies. Consider what is happening here in Asia. Every day we hear dire news about exports and industrial production—mirroring the remarkable collapse in global trade and industrial activity.

We have halved our Asian growth forecast for 2009, to about 2½ percent. Why? Because Asia’s open economies are especially export-dependent and therefore vulnerable to the ongoing decline in demand in the United States and Europe. So even though Asian countries did not originate this problem they are feeling its consequences intensely.

To contain this crisis we need a coordinated global response. We saw in 2008 that piecemeal responses are not enough. This does not mean that all countries should do the same things, or that there is a “one size fits all” solution. But policy responses have to take into account the interconnectedness of national economies, and the fact that decisions taken in one country can have profound effects on others. Protectionism is a clear danger. Let me give you an example.

Some countries are trying to make government support of banks conditional on their giving priority to domestic borrowers, to the detriment of financing across borders. This will hurt emerging economies, whose growth depends on access to foreign bank financing. It is protectionism in the financial markets, and its consequences could be as damaging and dangerous as the trade protectionism of the 1930s.

In fact, even without government intervention, we are already seeing a very sharp fall in financing for emerging markets.

These developments should leave no doubt that we need urgent action. We need financial market measures, in order to get credit flowing again. We need monetary and fiscal policy measures, to offset the abrupt fall in private demand. And we need liquidity support for some emerging market countries, to reduce the risk that growth in these countries grinds to a halt if key financing needs are not met. Let me take these issues in turn.

Restoring Stability to Financial Markets

Financial stability is essential to the recovery of the global economy. Policy makers have already acted to address the immediate threats to systemic stability, through massive liquidity support. They have also extended deposit insurance and other guarantees, something that we have learned from past crises, including the Asian crisis, is essential to maintain public confidence.

But more must be done to address the underlying lack of confidence in the solvency of the system, which stems from a lack of confidence that past losses have been properly recognized, and now also concern about new losses—extending well beyond real estate—as the economy turns down.

The task for governments is therefore to push the bank restructuring process forward—with an emphasis on cleansing balance sheets—using its authority to:

• Re-examine bank balance sheets on a worst-case basis, determine the viability of various institutions, and restructure them if required. Authorities need to be ready to respond as needed, including full-fledged intervention.

• Provide public support where necessary to banks that can be rehabilitated, in the form of capital, bad asset carve outs, and guarantees.

• Sell or wind-up insolvent banks quickly, depending on whether any franchise value remains.

• Establish new public resolution agencies to manage “bad assets” to maturity or sale. On this last point, the United States and Western Europe can learn from the previous experience of countries like Korea, Malaysia, Thailand, and also Sweden, which set up such agencies, and often recovered a lot of public money.

Even with these measures, it will take time to restore credit growth. They will also be expensive for governments. But you know very well that the costs of banking crises increase if problems are not addressed quickly. This is not the time for hesitation.

Supporting Aggregate Demand

Fixing the financial sector is essential but it is not enough, given the damaging feedback loop from weaker growth to financial stress. To restore aggregate demand we also need supporting monetary and especially fiscal policies. I have been really impressed with the speed and determination with which central banks have acted—not just the Fed and the ECB but central banks around the world.

(etc)

http://www.imf.org/external/np/speeches/2009/020709.htm

Speech By Dominique Strauss-Kahn, Managing Director of the International Monetary Fund

At the 44th SEACEN Governors’ Conference

Kuala Lumpur, Malaysia, February 7, 2009

Download the presentation (108 kb PDF)

***

also found in this presentation –

2009 IMF Projection of Deeper Recession than originally expected

***

Peter Morici described on CNN with Ali Velshi today that there are $600 Trillion in derivatives which is 5 x’s more than the actual economy – could I have made the note incorrectly – and some charts – info and facts that show the economic damage that has been done by these shadow economy products

That note was from CNN today, 04-22-10 at 2.30 pm – I will look up the transcript and see if I made the note correctly because my question is (if that is true that there are over $600 Trillion dollars worth of derivatives) then as part of the overall currency in the system, what does that do to the distributed assumed values of other assets, currency values, real property values, and other parts of the system? Never mind, just a thought.

– cricketdiane, 04-22-10

***

I’m so sick of hearing Republicans including Mr. Cox that heads up the New York Republican Party saying as he just did on BBC America World News that the financial industry might leave and go to Bangkok or London instead if the financial regulation and reform isn’t done right (to suit them.) – The fact is, they wouldn’t let them get away with this shit in London or Bangkok or in Kuala Lumpur or anywhere else. Check the IMF and other international sources of economic standards – they’ve had it with the American financial industry tactics that are opaque and shady which have diminished the financial stability of the entire system.

There has to come a point at which reasonable, prudent rules of the road are used as standards across the board which apply to make the system honorable, decent, fair and transparent or there will be no game at all because sooner or later, the credit crunch effect we’ve already seen will happen to an even broader and deeper arena. I know they don’t think that. I know they believe they’ve gotten away with it this time and made their profits free and clear as long as nobody rocks the boat and they will do it again provided that the rules stay the same and no one is truly the wiser for what has happened.

But what is the truth – every chart shows that the damage is deep and dear, that the values of stocks are way over-valued and that damages in the real economy across the US and Europe especially are still continuing in deep dramatic and life damaging ways to huge portions of the population.

They, (in the financial industry) have used our national resources with complete contempt and disregard then denied any responsibility for causing the financial crisis nor do they intend any change in the corrupt system they created which allowed it regardless of the harms that have been done.

Didn’t these Wall Street and banking and investment firms steal people’s life savings, their pensions, our state budget treasuries, our taxpayer revenues, our economic prosperity, our jobs, our businesses that have been bankrupted by it, foreclosed on our homes, caused our school budgets that are being cut because of it and diminished our ability to have jobs or businesses even into the future?

***